Developmental prospects in the global south are not constrained by geography or a lack of knowledge: rather, they are predominantly restricted by the structure of the global economy itself. The effects of this structure convey across a number of channels. Via sovereign debt, the financial channel sees public resources in the south extracted and dispatched into the pockets of investors. Tax avoidance and evasion schemes deployed by multinational corporations and wealthy individuals further deplete the public coffers while limiting industrial policy options. Phantom foreign investment distorts the reality of capital flows. Via the spectre of currency depreciation, the monetary channel often enforces austerity while threatening to deepen debt troubles. And the concentration of manufacturing capacity in East Asia combines with flatlining global demand to block avenues for development.

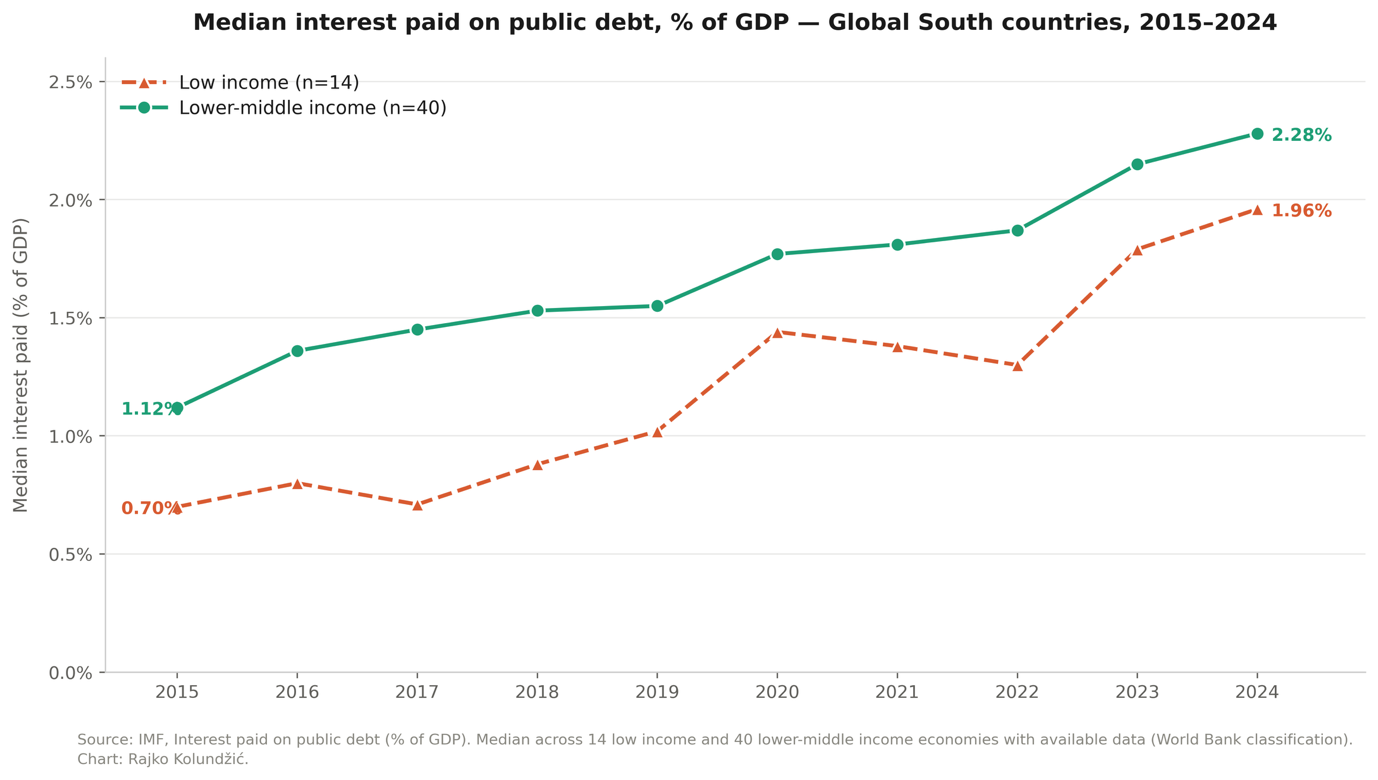

Debt Payments

At our present juncture, it is sovereign debt issues which are most immediately pressing in much of the Global South. For years, debt levels and interest payment have been on the rise. The effects of this are destructive. Outpacing spending on healthcare and education in some cases, rising debt payments have squeezed fiscal spaces and forced governments to divert resources away from investment in people and development. This stark reality illustrates a fundamental trade-off at the heart of many global south economies. Instead of constructing hospitals, supporting public education, or expanding social safety nets, public resources are transferred to creditors, a disproportionate share of which are foreign.

External events can also lead to increasing debt levels and payments. The most recent US-Israeli war on Iran is having large spill-over effects for the public finances of countries in the global south Due to the Strait of Hormuz deadlock, those reliant on imported energy and agricultural commodities like fertiliser and grain in particular face a double burden: With rising import costs depleting foreign reserves and borrowing rates rising, debt servicing becomes more difficult with each passing day.

Tax Abuse

Issues created by debt servicing are compounded by those introduced via eroding tax bases. The global north bears direct responsibility for the latter. Via influence over international tax rules and maintenance of preferred tax haven jurisdictions, the most powerful countries in the global economy (and the lawyers and accountants that populate them) have created a complex system enabling large-scale cross-border profit shifting. Indeed, over two-thirds of all global tax losses can be attributed to the global north members[1], underscoring a systematic failure of the international tax system to ensure that multinationals pay their fair share in proportion to their economic activity and profits within host countries. Recent estimates indicate multinational corporations shift around $1.42 trillion in profits into tax havens annually, causing governments to lose US$348 billion in tax revenue every year.[2] This has strongly undermined the ability of governments to raise revenue for its social and economic investment, causing significant deprivations in human rights and loss of life.[3]

Phantom FDI

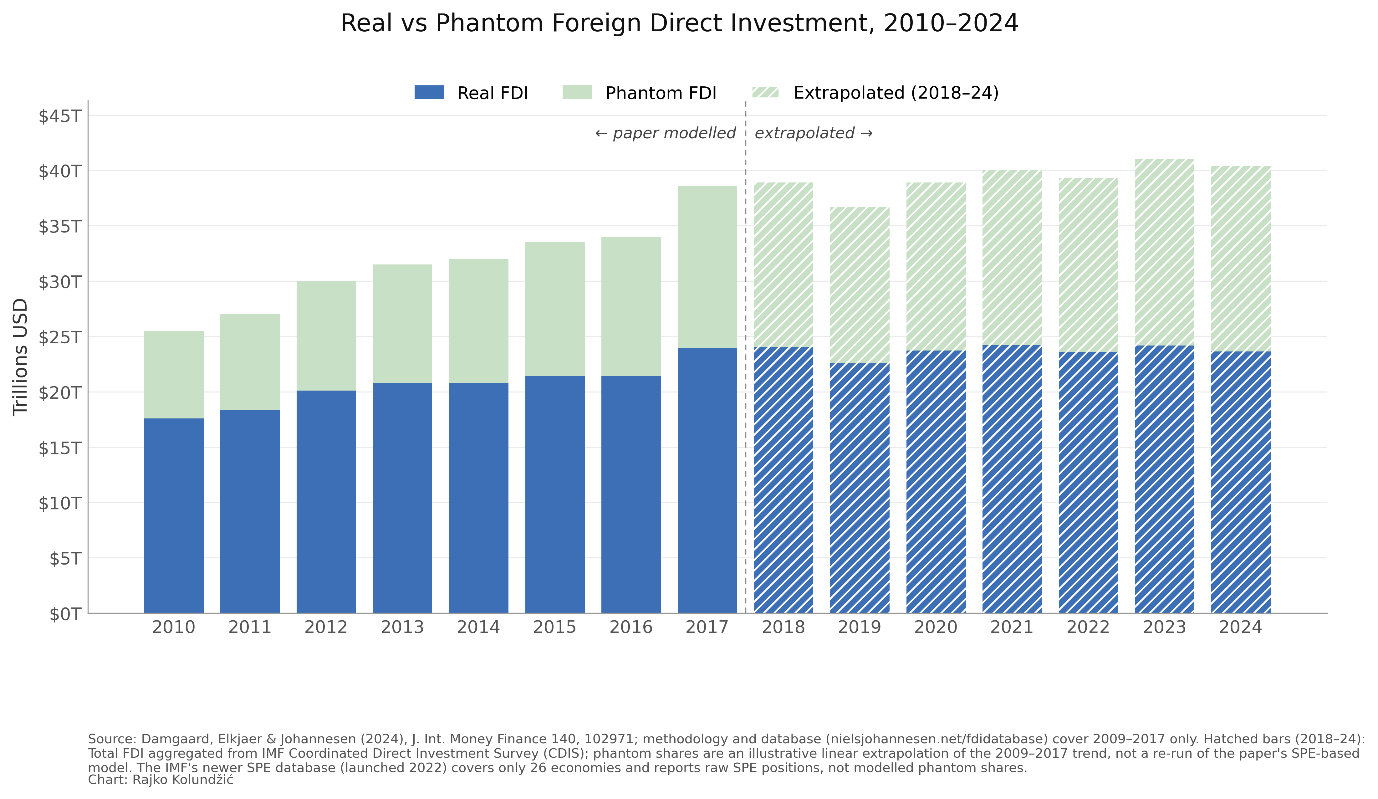

Compounding matters further is the dearth of investment capital being mobilised in the global north today. Foreign Direct Investment (FDI) was traditionally understood as a vehicle for long-term productive investment and assumed to make various contributions for host economies such as technology transfer, employment creation, and capacity building. Over recent decades, however, a different kind of FDI has come to dominate financial flows officially classified as FDI. This we call ‘phantom’ investment. It can be defined as financial transactions recorded as foreign investment but one that lacks in real economic substance. Materially, it often takes the form of assets being shifted between shell companies in tax havens to manipulate ownership details for tax avoidance purposes.

Unlike real foreign investment—which involves establishing lasting investment and thereby contributing to the host economy by way of local economic activity, supply chains and tax revenue— phantom FDI is a purely financial phenomenon. Approximately 40% of global FDI can be classified as phantom today, a figure which goes a long way toward explaining the global south’s struggles with job creation and climate resilience, amongst other things.

Currency Deprecation

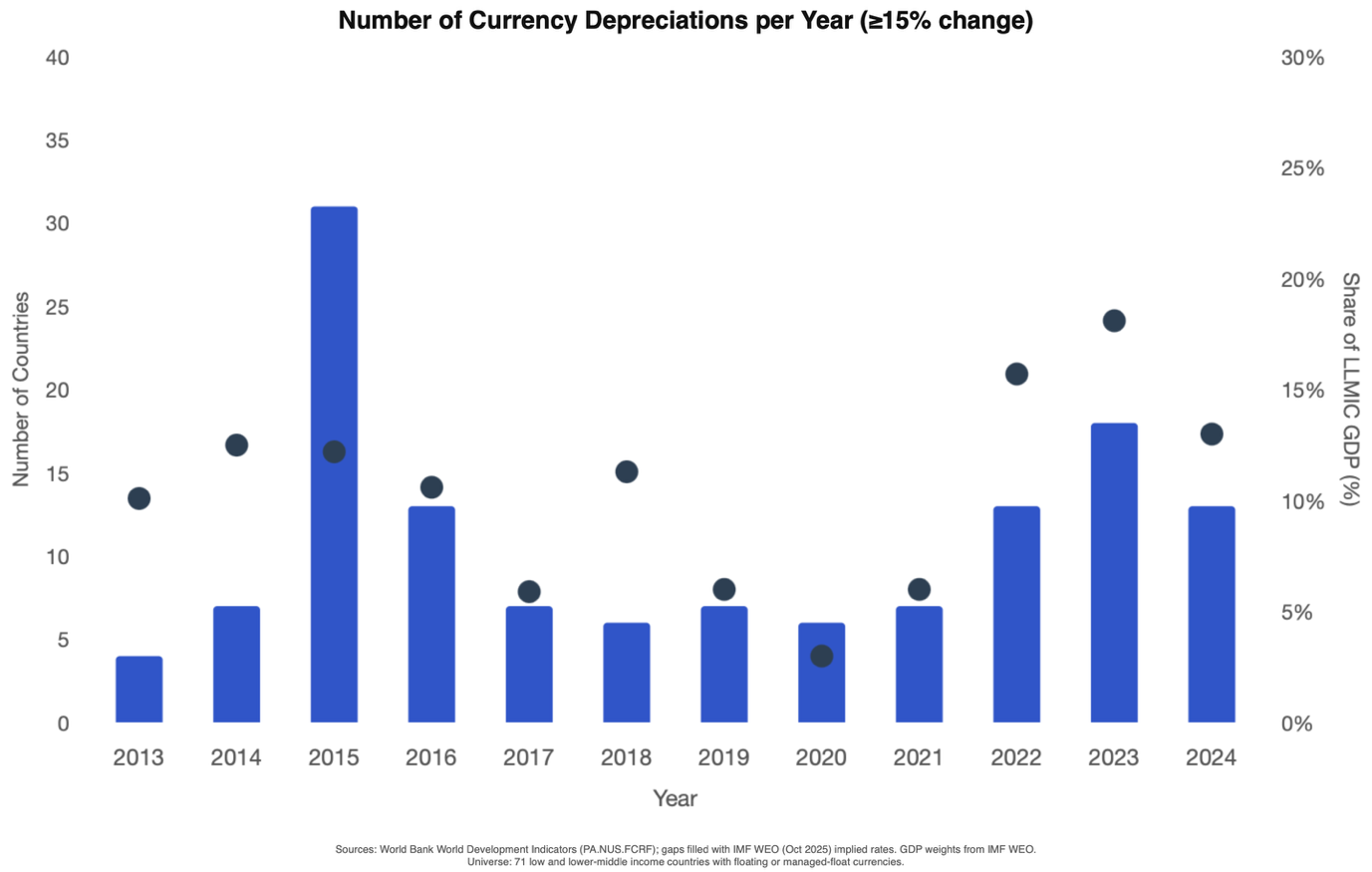

The workings of the global financial system also heighten prospects of currency depreciation, events that can have devastating economic effects. One of the key factors at play here is that fact that much of the global south, India included, issues a significant portion of their overall liabilities in foreign currency. This creates a structural vulnerability. Specifically, when financial conditions in the global north shift, currencies in the global south can come under pressure as capital rapidly exits the national economy. Where pressure leads to depreciation, a number of knock-on effects are introduced. Firstly, the cost of debt servicing rises as does the cost of imports in local currency. Together, these dynamics can strain national balance of payments to the point of breaking. Secondly, mobilising larger amounts of debt financing in order to pay back creditors implies making cuts to other public expenses. Typically, such cuts impact spending on health, education, and social protection.[4]

Recent years have seen the aggregate number of current depreciations decline. Nevertheless, the three-year average remains elevated in historical terms. And worrisomely, the picture today closely resembles what preceded the commodity price collapse of the mid 2010s, which was followed by a swift and pervasive spread of currency depreciations.

Pakistan’s example can illustrate what currency depreciation can mean in practice. There, repeated depreciations have driven up the cost of running business, raised the cost burden on energy production projects, reduced international market competitiveness, and made imports such as fertilisers, oil and machinery, significantly more expensive.[5]

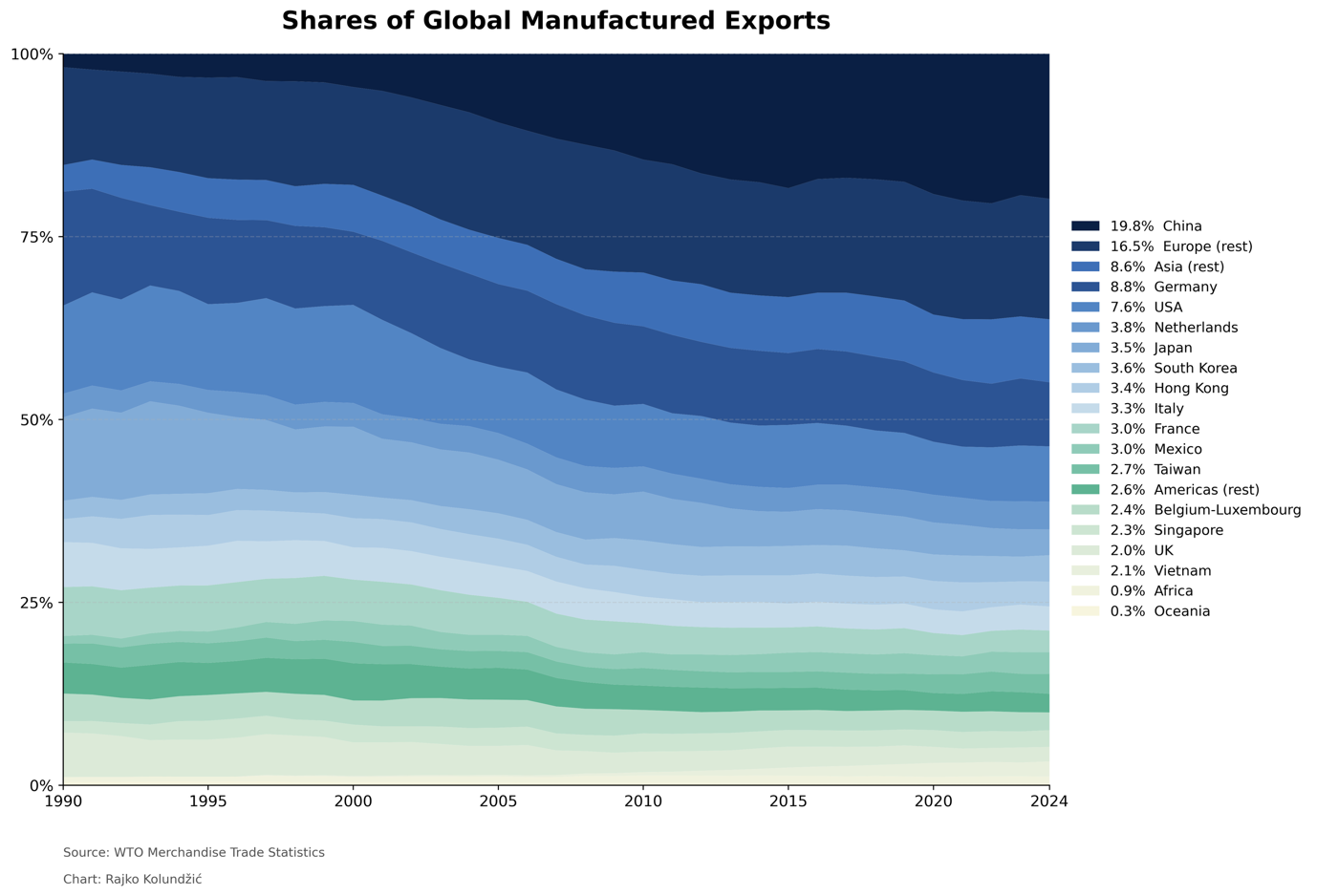

Asian Manufacturing Dominance

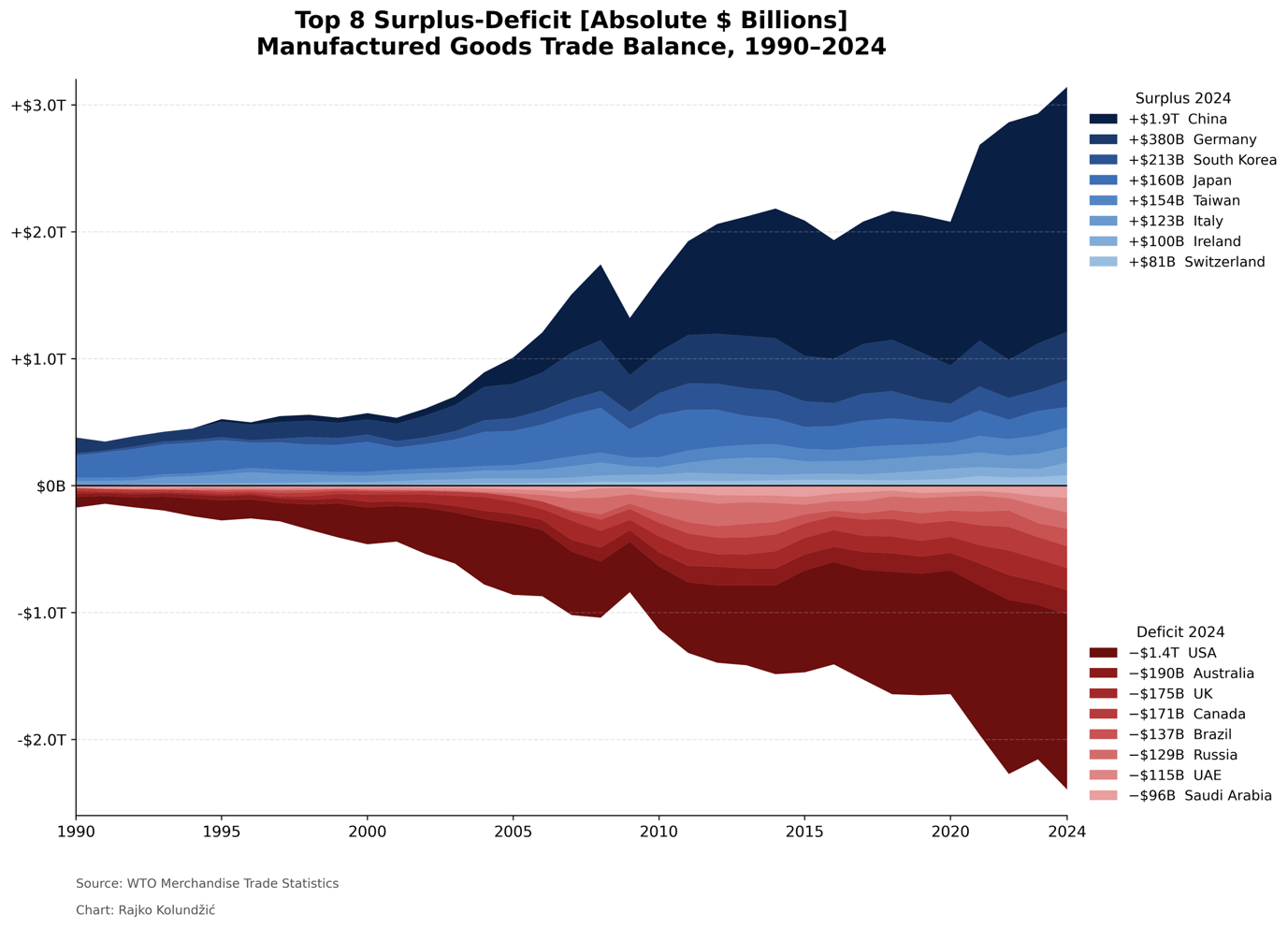

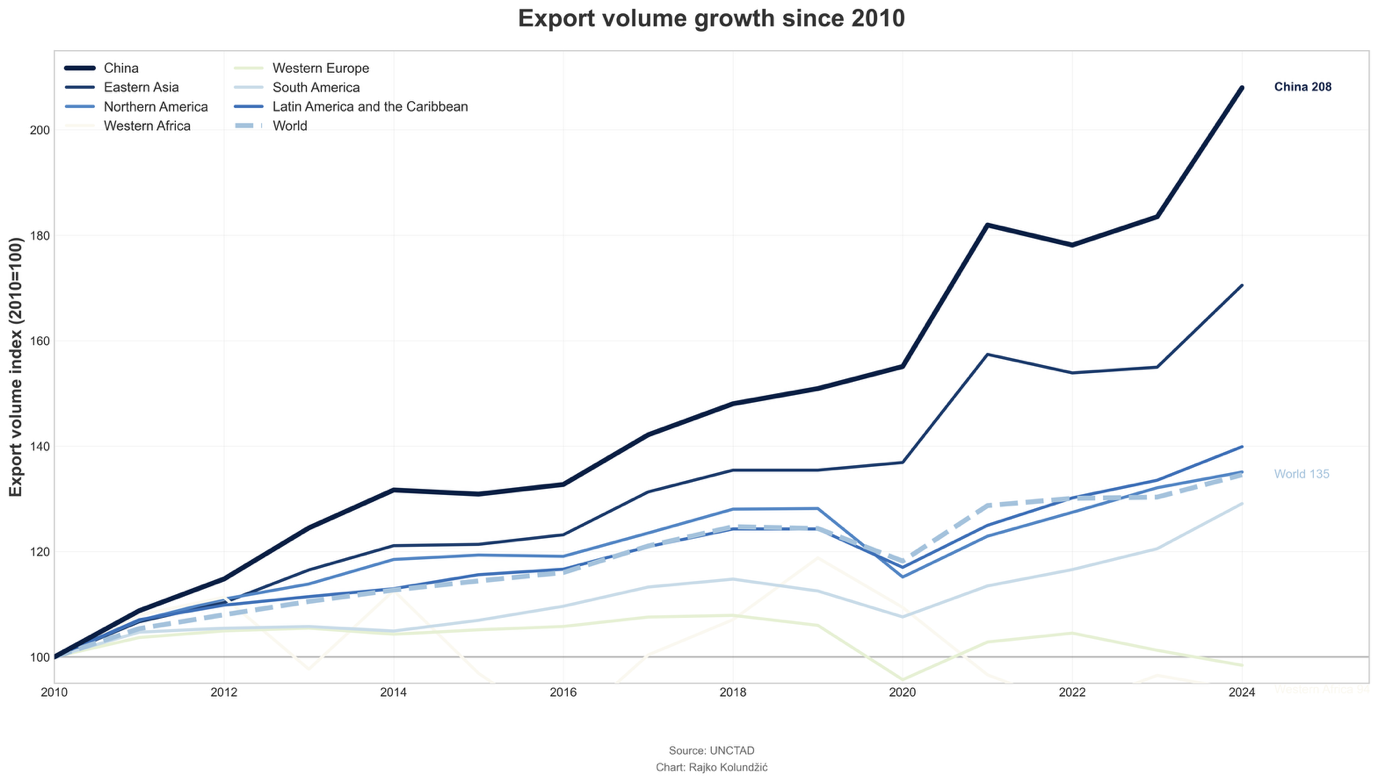

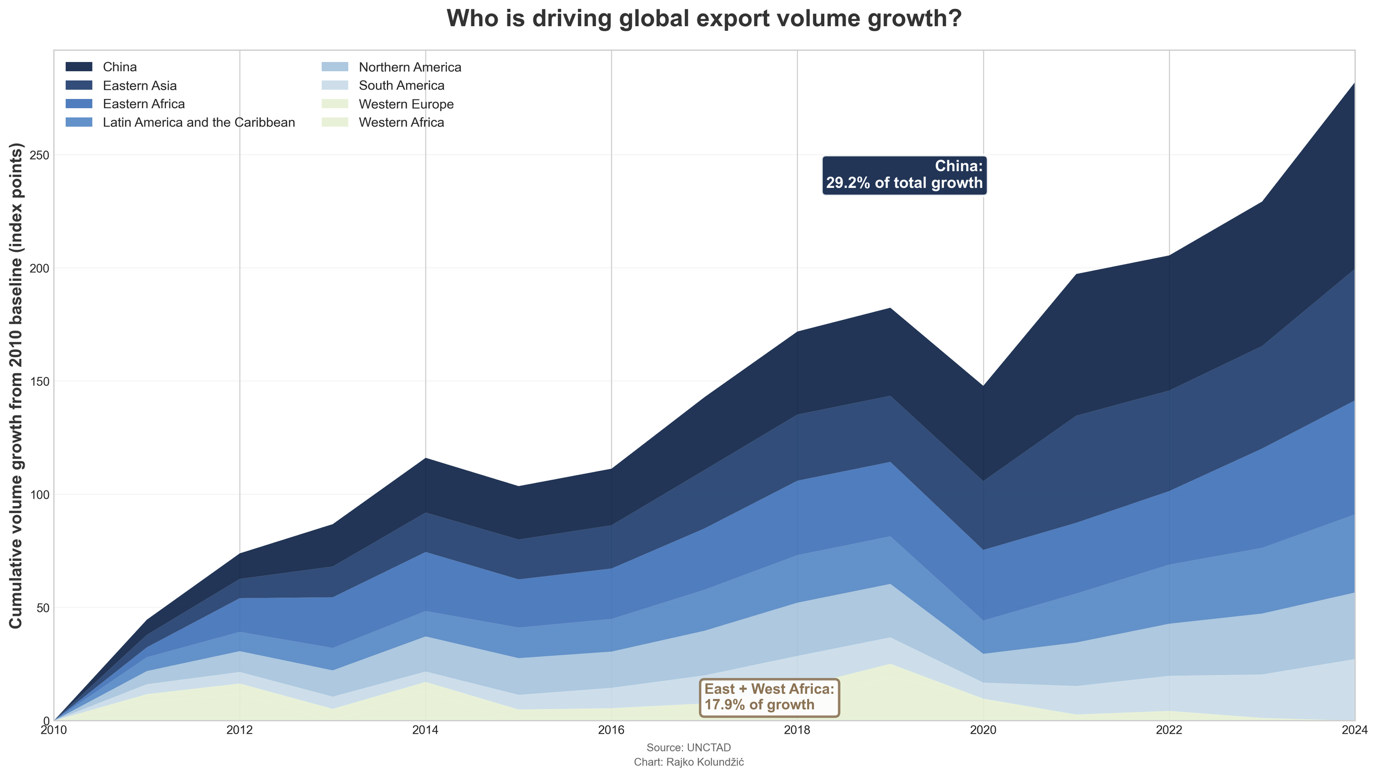

Amidst all this, the nature of global systems of production and exchange—centred on the dollar, a system of tax havens, phantom investment flows, and debt dynamics—only intensify the developmental constraints and prospects of the south. The examples of India and Pakistan attest to this well. By dint of these systems, each faces chronic currency vulnerability, commodity import costs denominated in dollars, and capital markets that punish current account deficits. In face of these conditions, the rational response is to accumulate reserves and pursue export surpluses: While not without costs—reserve accumulation deprives an economy of potential investment—such a strategy allows an economy to partially insulate itself from currency crises and punitive external creditors. But due to China’s successes on this front, export-led strategies are no longer especially viable for other members of the global south..

Increasingly, the entire global goods surplus concentrates in East Asia, while growth in Chinese import demand appears to be falling. By consequence, countries such as Ethiopia or Brazil are running out of the space for manufacturing-led industrialisation before they even climb the development ladder. Indeed, the south’s share of global export manufactures is now miniscule, the market dominated by East Asia, Western Europe, and North America.

The structure of global demand being what it is, there is simply no customer for the goods that a developing African or Latin American nation would need to sell in order develop healthily. A larger question therefore begs asking: At this stage, what developmental project is available to countries in the global south—the demographic future of humanity? What is the way out of a future burdened by financial crisis, subordination, and climate disruption?

Conclusion

Viewed in full, a self-reinforcing system of subordination comes into view. On the fiscal-monetary front, a country that loses tax revenue due to avoidance and evasion schemes has less fiscal buffer when its currency depreciates. Facing a depreciated currency, states bear higher debt service costs, which forces cuts that erode the state capacity needed to collect tax. Weaker tax collection means greater dependence on external borrowing, which increases debt vulnerability (and thereby spikes currency fragility). And so on and so forth. On the production side, meanwhile, a system of accumulation concentrates manufacturing capacity in a handful of regions just as profits concentrate amongst the intellectual property holders of the global north. As demand weakens at a planetary scale, all roads to southern development become blocked.

Such a globalized economy did not emerge from nature. Rather, it was assembled over time as elites—those of the north first and foremost, but their allies in the south as well—put their own interests above those of publics. A different global economy could be reassembled. Through different allocations of the IMF’s Special Drawing Rights, a new Bretton Woods system designed to meet the needs of the global south, the cancellation of unsustainable debt, establishment of a new rights-based multilateral tax system, and reform to the infrastructure allowing phantom investment, a different world could be made. But achieving this won’t be easy: The struggle will be transnational in scale—requiring popular forces from around the globe to unite in solidarity.

Photo Credit: “Man protesting the scarcity of bread rations, suffers tear gas exposure.” by Alisdare Hickson, CC BY-SA 2.0

[1] Rachel Etter-Phoya et al., “Profit Shifting from Nigeria to Europe: The Impact on Human Rights,” ed. Roojin Habibi, PLOS Global Public Health 5, no. 3 (March 19, 2025), https://doi.org/10.1371/journal.pgph.0004218.

[2] Tax Justice Network, “The State of Tax Justice 2024,” Tax Justice Network, 2024, https://taxjustice.net/reports/the-state-of-tax-justice-2024/.

[3] Rachel Etter-Phoya et al., “Profit Shifting from Nigeria to Europe: The Impact on Human Rights,” ed. Roojin Habibi, PLOS Global Public Health 5, no. 3 (March 19, 2025), https://doi.org/10.1371/journal.pgph.0004218.

[4] Blessy Augustine and Lakshmi Kumar, “Original Sin, Currency Depreciation and External Debt Burden: Evidence from India,” International Journal of Economics and Financial Issues 10, no. 3 (April 20, 2020): 58–68, https://doi.org/10.32479/ijefi.9487.

[5] Saif Ullah and Haitham Nobanee, “Decoding Exchange Rate in Emerging Economy: Financial and Energy Dynamics,” Heliyon 11, no. 2 (January 2025): e41995, https://doi.org/10.1016/j.heliyon.2025.e41995.