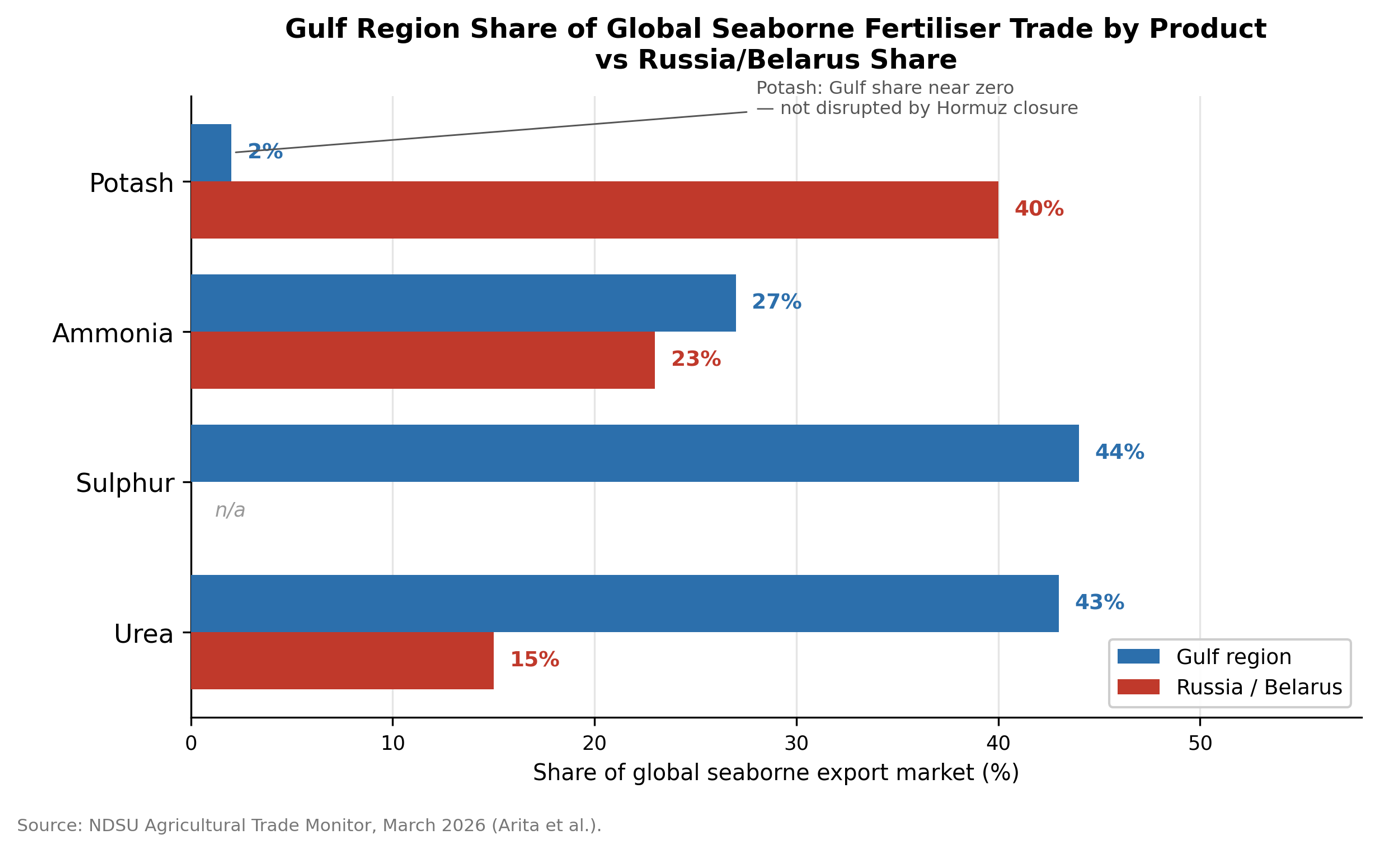

Apart from a humanitarian catastrophe, the current war on Iran is wreaking havoc on global supply networks, including hydrocarbons and fertiliser. To appreciate why, consider that the Strait of Hormuz is not only a bottleneck for about a fifth of global oil and liquefied natural gas but also approximately 43 percent of globally traded seaborne urea, 44 percent of global seaborne sulphur, and over a quarter of the world’s ammonia exports.[1] As such, the war threatens energy markets just as it threatens to precipitate an agrarian crisis whose consequences will be felt in the food markets of the Global South well into 2027.

The Strait of Hormuz as Fertiliser Chokepoint

The role of the Persian Gulf in global food production is manifold. As Vaclav Smil puts it, modern agriculture is “subsidised” with fossil fuels. Hydrocarbons enter the supply chain both directly as energy sources—in the form of tractors, trucks, irrigation, refrigeration—and indirectly as feedstock for fertilisers. Key in the second regard is use of natural gas in the Haber-Bosch process for producing ammonia. In addition to hydrocarbon fuel and feedstock, the Gulf region also produces sulphur as a byproduct of hydrocarbon processing, which is needed in the form of sulphuric acid for processing phosphate, of which Saudi Arabia is a major producer.

Due to its arid climate, the Gulf uses little fertiliser domestically and exports most of the finished products (and raw and intermediate fertiliser inputs) it produces. As a result, four Gulf states feature in the top ten global urea exporters.[2] Bahrain’s refineries export sulphur to processors from Morocco to China. Meanwhile, Saudi Arabia’s state-owned mining company, Ma’aden, is undertaking one of the largest phosphate production expansions in the world, targeting nine million tonnes of annual capacity by 2027.

Production Shut-ins and Cascading Consequences

In peacetime, the Gulf’s geography is a supply chain advantage, with sea routes connecting the world’s largest nitrogen and phosphate suppliers to the world’s largest agricultural economies in India, Brazil, and Southeast Asia. But under present conditions, the same geography presents a dangerous point of failure.

Commercial traffic through the Strait is currently down to about twelve Iran-approved passages per day.[3] Insurers suspended war-risk coverage for tankers attempting passage following Iranian warnings and attacks on multiple vessels. The few ships that are granted passage pay a fee of $2 million to Iran. The result is an effective embargo on the Gulf’s entire export economy, including fertilisers. Storage facilities at Ras Laffan and Mesaieed are running out of capacity, forcing production cuts irrespective of whether physical damage has yet reached the plant gate.

The immediate supply loss has been large and, crucially, affects both nitrogen and phosphate, two of the three critical fertiliser components (the third being potassium). QAFCO declared force majeure following the Iranian strike on QatarEnergy’s LNG facilities at Ras Laffan, which interrupted the gas feedstock supply.[4] This removes roughly 14% of the world’s urea supply. Bahrain’s Bapco refinery, among the Gulf’s major sulphur exporters, has also declared force majeure. Ma’aden continues to operate but faces the same constraints as feedstock production is disrupted and its main export corridor, the Strait of Hormuz, remains essentially closed.

What distinguishes this crisis structurally from the 2022 Russia-Ukraine shock is the cascade effects being introduced via sulphur, of which the Gulf is the single largest exporter. Sulphur has no substitute in fertiliser production as sulphuric acid is used for converting phosphate rock into diammonium phosphate (DAP) and monoammonium phosphate (MAP), two essential phosphate fertilisers. Morocco’s state-owned mining company, the Office Chérifien des Phosphates (OCP), is the world’s largest phosphate producer with about 70% of global phosphate reserves and is geographically removed from the war on Iran. Yet, it normally imports approximately 3.7 million metric tonnes of sulphur annually from the Persian Gulf.[5] Without it, the OCP cannot process rock into usable product at scale. China, itself a major phosphate exporter—and one that had already imposed export restrictions on DAP and MAP before the war—faces a similar input constraint: it imports approximately 3.8 million tonnes of Gulf sulphur per year, and has already halved its sulphuric acid export schedule.[6]

As a result, three of the world’s five major phosphate producers — Saudi Arabia, China, and Morocco — face simultaneous supply pressure through three different channels: physical blockade, self-constraining export controls, and input shortage, respectively. Due to all roads to phosphate fertilizer running through Gulf suphur, the apparent geographic diversification of world phosphate production is no such thing at all.

Price Movements and Comparison with 2022

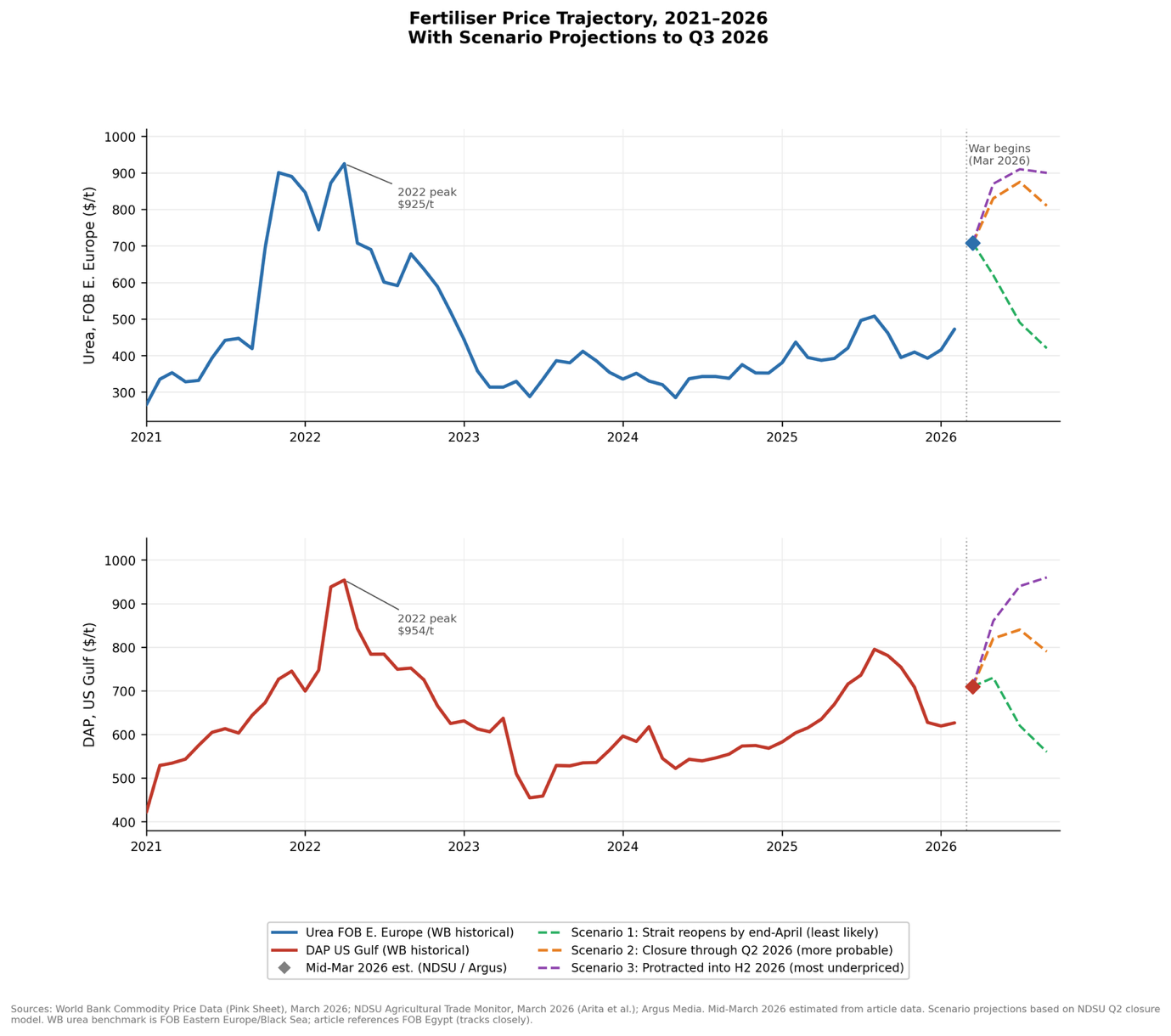

Price movements since the opening of the war reflect these structural pressures, though markets have been slower to price the fertiliser shock than the energy shock. In under three weeks, urea FOB Egypt had risen approximately 50%, mirroring price movements in Southeast Asian granular urea.[7] Ammonia FOB Middle East had risen twenty-four percent. DAP at US Gulf ports had crossed $700 per tonne by min-March, approaching the level of Fitch projected at end of year.

The comparison to 2022 is instructive: that year, urea ultimately reached approximately $925 per tonne and DAP exceeded $1,000 per tonne. Current prices remain well below those levels, but the underlying drivers suggest continued upward pressure. Research from North Dakota State University’s (NDSU) Agricultural Trade Monitor indicates that a Strait closure persisting through the second quarter could push DAP past $800 per tonne and urea toward $850–900 per tonne.[8]

For farmers, the comparison to 2022 obscures an asymmetry that makes the current situation potentially worse than nominal price figures suggest. In 2022, the shock to fertiliser supply arrived alongside a large and simultaneous shock to grain supply: Russia and Ukraine together account for around 30% of global wheat exports, so grain prices rose sharply, giving farmers elevated revenue which could partly offset elevated input costs. But in this instance, the Gulf is, of course, not a grain producer. By consequence, fertiliser prices are today rising against flat or slightly declining grain prices, meaning that the cost-price squeeze, unlike 2022, offers no offsetting improvement to crop revenues. This asymmetry may exacerbate the humanitarian implications of the current crisis compared to those of 2022, even if fertiliser prices do not reach the same peak.

A further distinction bears mentioning, too. In 2022, despite the war, Russian and Ukrainian fertiliser exports were able to be at least partially rerouted in order to reach market. Contrarily, the Gulf’s production is effectively trapped in the Strait. Ships cannot get out, rerouting via land bypasses is inadequate and expensive, storage is filling, and production plants are cutting production, meaning that this time, there is no logistical workaround for getting supply to global markets.

Most Exposed Importers

The fertiliser shock has varying effects depending on the geography of import dependence and the timing of planting cycles.

India is arguably the most exposed large importing economy in the world. It is the world’s single largest importer of DAP fertiliser, accounting for 28.7% of the international market by volume. Saliently, it received more than half of total fertiliser imports (9.7 million tonnes) from the Persian Gulf in 2024.[9] India’s two largest phosphate suppliers are Saudi Arabia (24% of DAP imports) and Morocco (22%).[10] Furthermore, the country imports approximately $2.2 billion worth of urea annually, with Oman and Saudi Arabia as leading suppliers. And when it comes to urea, it is worth noting that sharply rising LNG prices have created a feedstock shortage and forced production cuts, with the Indian Farmers Fertiliser Cooperative already reducing output.

If one searches for optimism, there are some factors which could mitigate the effect of the fertiliser squeeze on Indian food production. Domestic production offers partial relief since India operates thirty urea manufacturing plants. The government has reported that its buffer stocks are above last year’s levels (urea up 10.7%, DAP up 105% year-on-year).[11] Moreover, the Indian government shields farmers through fertiliser price ceilings, so that price surges will primarily hit government finances. But the kharif season, India’s most important planting window, opens in June and July. If supply remains disrupted through May, India will inevitably face a genuine phosphate shortage at a critical moment.

Brazil’s exposure is structurally even more acute. It is the world’s largest fertiliser importer, bringing in approximately 46 million tonnes in 2025.[12] Imports cover over 85% of domestic consumption as the country boasts no significant capacity to domestically produce nitrogen fertiliser. Roughly half of those imports normally transit the Strait of Hormuz. Making matters worse is the question of timing: Brazil’s soybean season completes its 2025-26 harvest at the time of writing, and farmers will begin purchasing inputs for the 2026-27 season in the second and third quarters.[13] Here, forward-looking indicators paint a distressing picture. Brazil’s urea imports have already fallen by 33% compared to the same period last year. The repercussions could be severe for Brazil, a country where soybeans underpin national export earnings, but also downstream as so many global livestock feed chains depend on Brazilian soybean feed, particularly Chinese livestock.

Southeast and South Asia present a similar exposure profile during the northern hemisphere planting season. As mentioned above, China has responded to the crisis by extending its phosphate export restrictions through August, which has removed a significant short-term relief valve for Southeast Asian buyers: Indonesia, Vietnam, and Thailand now face compounding supply gaps issued forth from the Persian Gulf and China simultaneously. In South Asian countries especially dependent on Gulf supply, production halts have already occurred: Pakistan and Bangladesh have seen complete stoppages at major domestic fertiliser facilities as gas feedstock has dried up. Sri Lanka, which was already food-vulnerable pre-war, faces renewed pressure, too.

Europe occupies a structurally different position but is not insulated. Gas-based European fertiliser plants, already curtailed or shut down by the combination of the sabotage of the Nordstream II pipeline and EU sanctions on Russian gas, face renewed cost pressure: Dutch TTF benchmarks rose more than fifty% in the first two weeks of the conflict. German farmers were paying around €550 per tonne for urea by mid-March while receiving €168-176 per tonne for feed wheat — a cost-price squeeze that leaves little margin for absorbing further input inflation. For phosphate specifically, Europe depends primarily on Morocco, Russia, and (pre-war) the Gulf. However, as mentioned above, Morocco’s OCP sits downstream of Gulf sulphur, constraining its own output. To mitigate the impact on European agriculture, the European Commission has proposed temporarily suspending tariffs on third-country fertiliser imports and a temporary waiver of the Carbon Border Adjustment Mechanism (CBAM) on fertilisers, although the latter motion was defeated at a recent meeting of European agriculture ministers. However, some European suppliers had stocked up on fertilisers before CBAM came into effect on January 1 this year, meaning that some buffer stocks were in place to soften the blow of the war.[14] The infighting about fiscal measures for fertilisers thus seems to mirror the political economy underlying Europe’s energy dependency problem.

Opportunities for and Limits of Mitigation

The market’s responses to supply disruption have followed predictable channels, none of which inspire great confidence. The most frequented channel is substituting the fertiliser furnished by Gulf suppliers for the product of other countries. Indeed, India’s Fertiliser Ministry already reported “strong responses” to import tenders from Russia, Morocco, and Belarus.

Similar to the energy crisis, Russia is the most obvious beneficiary and the most available large-volume alternative supplier of fertilisers. Russia and Belarus together account for around 40% of global potash exports (although the Gulf is not a major potash producer and there is thus no major shortage), 23% of ammonia, and 14-16% of urea, and their export logistics are unaffected by the Gulf war.[15] West African importers — Nigeria, Ghana — have already begun to pre-purchase Russian fertilisers for the third quarter of 2026.[16] Importantly, Russia’s food and fertiliser exports are exempt from Western sanctions, giving it full freedom to expand into these markets. The diplomatic relationships being established in this crisis will shape the geopolitics of fertiliser supply for years. For Russia, the outlook shows increased diplomatic leverage, particularly in Africa and the Global South which may be further enhanced if emergency exemptions on Russian oil and gas export sanctions go into effect.[17]

However, Russia faces three constraints that prevent it from making up for all the shortfalls of Gulf production. First and most fundamentally, Russia is not large enough to replace the estimated sixteen million tonnes of trapped Gulf annual capacity at short notice. Second, the Russian spring planting season creates competing demand, which has already meant that export licences for ammonium nitrate are suspended until late April. (More general nitrogen export caps have been in place since December 2021.) Third, Russian production cannot be expanded quickly: new export capacity will need wait for 2027.[18] Fourth, Ukrainian drone strikes on industrial sites have significantly impacted Russian supply. In addition to the disruption of oil and gas production facilities, the February 2026 strike on Acron’s Dorogobuzh plant disabled approximately 11% of Russian ammonium nitrate capacity until at least May.[19]

Morocco’s OCP is the other frequently cited alternative. Its geographical distance from the supply disruption, enormous phosphate reserves, and the large-scale capacity expansion underway (targeting 20 million tonnes by 2027) have all been lifted up as a source of hope. In fact, OCP has already executed significant phosphate sales to Latin American markets at elevated prices — an April shipment of 90,000 tonnes of MAP and TSP to Latin America was priced at $800-820 per tonne cfr, a sharply elevated price that signals how tight markets already are.[20] The US has likewise eased duty restrictions on OCP imports, treating Morocco as a strategic supply alternative. But in the end, the OCP’s ability to balance out the market is penned in by the sulphur shortage. Some buffer stocks and alternative sulphur sources exist (Canada, Kazakhstan), but re-routing supply at this scale will take months and increase input costs drastically.

A significant institutional development on 27 March could offer some near-term relief. The UN Secretary-General announced a task force to establish a humanitarian passage mechanism for fertiliser and agricultural goods through the Strait, modelled on the Black Sea Grain Initiative.[21] Iran has stated it will “facilitate and expedite” humanitarian aid through the Strait, and has already granted passage to vessels from China, Russia, India, Iraq, Pakistan, and Bangladesh.[22] The precedent is meaningful as the first significant diplomatic movement in four weeks of conflict. The material effect, however, remains uncertain. The Black Sea Grain Initiative’s own record is a cautionary template: it proved effective initially but was progressively undermined. In addition, the mechanism only addresses one channel, fertiliser exports from the Gulf, not intermediate products like sulphur.

Behind all mitigation measures lies the same absence: there is no international strategic fertiliser reserve equivalent to the IEA’s oil stockpile. Governments can release food stocks, waive tariffs, and issue emergency financing (and several are doing so) but no administrative measure substitutes for physical supply that is not moving.

Outlook

The war on Iran is already wreaking havoc on global economies through the double channels of hydrocarbon and fertiliser supply shocks, with ripple effects on global food prices from Europe to China. For the Global North, this will entail a variable degree of stagflation, a cost of living crisis, and rising inequality. For the Global South, it will mean food insecurity and a looming debt crisis. The severity of these outcomes will depend on the duration of the war and the ensuing disruption and destruction of supply.

Three trajectories today stand before us, each pointing in very different directions. In the least likely scenario, a negotiated ceasefire and Strait reopening in the coming weeks would allow partial restocking ahead of the critical planting windows in South and Southeast Asia. Fertiliser prices would remain elevated as disruption to forward contracts and insurance markets needs time to resolve, but the supply gap would be limited. Current price levels (DAP at ~$700/t, urea up ~50%) would persist into the third quarter before retreating. The 2022 peak levels would not be reached. Agricultural output loss would be manageable, concentrated in the regions least stocked at the war’s outset. Structural diversification toward alternative suppliers would accelerate, but a genuine food security emergency would be averted. Even in this optimistic scenario, it does bear mentioning that more distant horizons would remain threatened, as certain Gulf infrastructures, such as QatarEnergy’s Ras Laffan facilities, will take years to be fully restored.[23]

A more probable scenario is Strait closure through the second quarter. In this case, the kharif planting window in India and the soybean purchasing cycle in Brazil both face genuine supply gaps. NDSU projects DAP above $800 per tonne and urea approaching $850-900 per tonne under these conditions — approaching but not yet matching 2022 peak levels, though with a more damaging farm-margin effect given the absent grain price offset. The World Food Programme estimates that an additional 45 million people worldwide could face acute food insecurity if the war does not end by mid-2026 and oil prices remain above $100 per barrel.[24] Critically, this scenario also implies significant yield losses in the 2026-27 harvest cycle, as farmers facing a combination of supply constraints and elevated prices apply less fertiliser. The consequences of reduced application will not be immediately visible: they show up in harvests months later, by which point the war may be over and market attention will have moved on.

The third scenario, a protracted conflict extending into the second half of 2026, is the one that current market pricing most consistently underestimates, even though both sides remain in a logic of escalation rather than negotiation. Iran’s hold on the Strait is its most powerful deterrent in the absence of nuclear capacity, and there is limited incentive to surrender it without durable resolution of the underlying causes of the conflict, which include the broader question of Iran’s security environment and sanctions relief.

Meanwhile, the Gulf’s fertiliser production infrastructure, which includes large, capital-intensive complexes that take months to bring back online after extended shutdowns, is increasingly at risk of physical damage if the conflict continues. Indeed, this scenario would also entail a major intensification of the conflict, with U.S. landing operations, followed by an Iranian response, including large-scale destruction of GCC hydrocarbon and logistics infrastructure, mining the Strait of Hormuz, and blocking of the Bab al-Mandeb strait by the Houthis.[25] The longer the war lasts, the more the distinction between a temporary supply disruption and structural capacity loss narrows. If this should be the door we walk through, the fertiliser crisis transitions from an acute shock to a durable impairment of global agricultural supply capacity — with consequences that will not be remedied by any reserve release or emergency import tender. In such an eventuality, the knock-on effect will be to greatly compound the food security pressures already accumulating from climate disruption and post-pandemic supply chain fragility.

Such a future should also be read against a background that the 2022 crisis does not provide. The Russia-Ukraine shock was a disruption to grain and fertiliser trade, severe but bounded. The current crisis operates through two distinct channels, firstly, LNG/nitrogen/urea and phosphate, secondly, sulphur. Markets are aware of this confluence, but have so far priced in a short war. The evidence suggests they may be disappointed.

Photo Credit: Lisa Leonardelli, “Qatar Producing Natural Gas” (2009)

[1] NDSU Agricultural Trade Monitor, March 2026 (Arita, Chakravorty, Kim, Lwin, and Steinbach), Center for Agricultural Policy and Trade Studies, North Dakota State University. Full text: https://ageconsearch.umn.edu/record/396250

[2] Gulf Petrochemicals and Chemicals Association: https://www.gpcachem.org/wp-content/uploads/2024/04/Product-in-focus-UREA.pdf.

[3] Windward: https://windward.ai/blog/four-weeks-into-the-iran-war/.

[4] QatarEnergy force majeure statement, 4 March 2026: https://english.alarabiya.net/business/energy/2026/03/04/qatarenergy-announces-force-majeure-following-iran-attacks-statement.

[5] NDSU Agricultural Trade Monitor, March 2026; Morocco World News, “Strait of Hormuz Closure Threatens Morocco’s Fertilizer Production, Exports,” 17 March 2026.

[6] NDSU Agricultural Trade Monitor, March 2026.

[7] Argus Media data, reported in CNBC: https://www.cnbc.com/2026/03/25/fertilizer-price-iran-war-food-security-inflation-urea-potash-nitrogen-farmers.html.

[8] NDSU Agricultural Trade Monitor, March 2026.

[9] Ibid

[10] Indian Ministry of Chemicals and Fertilizers: https://www.pib.gov.in/PressReleasePage.aspx?lang=1&PRID=2237491®=3

[11] Ibid

[12] Reuters: https://www.reuters.com/business/brazil-sounds-alarm-fertilizers-price-spike-spurs-cheaper-alternatives-2026-03-18/

[13] Reuters: https://www.reuters.com/sustainability/brazils-agrion-aims-make-500000-metric-tons-fertilizer-per-year-waste-sugarcane-2026-03-11/

[14] Global Banking and Finance: https://www.globalbankingandfinance.com/eu-resists-french-request-pause-carbon-border-tax/, RTÉ: https://www.rte.ie/news/europe/2026/0330/1565867-fertiliser-eu-tax/

[15] Industry data on Russian/Belarusian fertiliser exports; Western Producer / AgCanada, March 2026: https://www.agcanada.com/daily/fertilizer-markets-tighten-as-russian-exports-hit-capacity-limits

[16] Reuters: https://www.reuters.com/business/energy/russian-fertiliser-makers-cant-offset-potential-iran-related-supply-crunch-2026-03-06/

[17] Carnegie Endowment for International Peace, March 2026: https://carnegieendowment.org/emissary/2026/03/fertilizer-iran-hormuz-food-crisis

[18] Reuters: https://www.reuters.com/business/energy/russian-fertiliser-makers-cant-offset-potential-iran-related-supply-crunch-2026-03-06/.

[19] Moscow Times, 25 February 2026: https://www.themoscowtimes.com/2026/02/25/ukrainian-drone-attack-on-smolensk-region-fertilizer-plant-kills-7-a92043

[20] Morocco World News, “OCP Ships 90,000 Tonnes of Fertilizers to Latin America,” March 2026: https://www.moroccoworldnews.com/2026/03/282848

[21] Bloomberg, 27 March 2026: https://www.bloomberg.com/news/articles/2026-03-27/un-creates-task-force-aimed-at-addressing-hormuz-closure; UN News: https://news.un.org/en/story/2026/03/1167182

[22] Euronews, 27 March 2026: https://www.euronews.com/2026/03/27/iran-says-it-will-facilitate-and-expedite-humanitarian-aid-through-strait-of-hormuz

[23] Al Jazeera: https://www.aljazeera.com/news/2026/3/20/qatarenergy-ceo-says-warned-us-industry-officials-against-attack-on-energy.

[24] WFP press release, March 2026: https://www.wfp.org/news/wfp-projects-food-insecurity-could-reach-record-levels-result-middle-east-escalation; UN News: https://news.un.org/en/story/2026/03/1167147

[25] Al Jazeera, “Houthis open new front in Iran war: Will Yemeni group block Bab al-Mandeb?”, 29 March 2026: https://www.aljazeera.com/news/2026/3/29/houthis-open-new-front-in-iran-war-will-yemeni-group-block-bab-al-mandeb